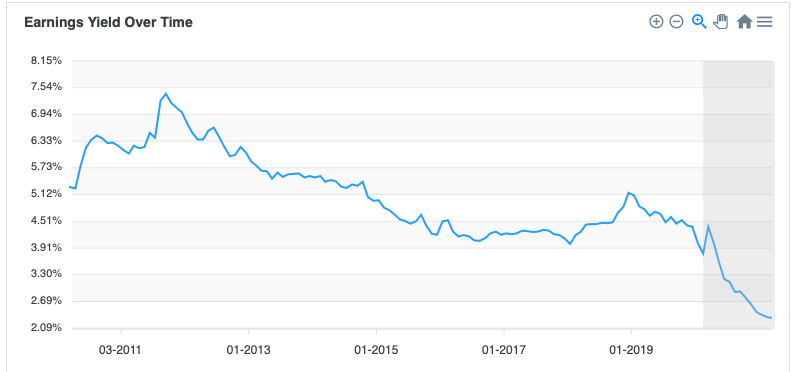

Beware the Steep Curve

Ignore Rate & Inflation Risk at Your Own Peril

All you need to understand when it comes to the big hoopla about the Fed/rates and investing: Pay attention to what happens when you move from left to right on the curve above.

Notice the change in slope (first derivative). It’s extremely high at low rates (approaches infinity as you move left to zero rates) and it falls rapidly as you move to higher rates (technically it’s less negative, but we only care about its magnitude or absolute value).

If you are buying a financial asset today, it’s likely that the notion of persistently low rates is implicitly priced in:

Due to recency bias, there is plenty of skepticism regarding rates rising in the future. As a result, assets generating very small or even zero cash flows (such as crypto) are priced accordingly. If this view is shattered by reality, asset prices will move rightward on the steep curve and Fools will learn the hard way…

Buffett and Munger hinted on this over the weekend:

“It's a fascinating time. We've never really seen what shoveling money in on a [fiscal] basis [like] we're doing it, following a monetary policy of something close to zero percent interest rates. It is enormously pleasant. But in economics, you can never do only one thing. You always have to say ‘and then what?’

It causes stocks to go up, it causes business to flourish, it causes an electorate to be happy, and we'll see if it causes anything else…”

—Warren Buffett, 2021 Berkshire Annual Meeting

Sustained Inflation Would Force the Fed to Raise Rates

Now consider the dual mandate of the Federal Reserve:

Stable Prices

Maximum Sustainable Employment

Read that again. Despite all the ruckus about J Pow pumping up stonks, the Fed doesn’t really care about stock prices. The Fed only really cares about price stability (avoiding high inflation and deflation) and avoiding excess unemployment. That’s it.

The Fed’s major tool to manage these? Interest rates. So, if prices excessively rise, where do you expect interest rates to go? Will the Fed have any choice? And no, the Fed will likely not have to worry about rising rates affecting employment as excess capacity will be soaked up by surging demand because the underlying cause of inflation will be unrestrained consumption due to the unique economic consequences of the pandemic and subsequent recovery…

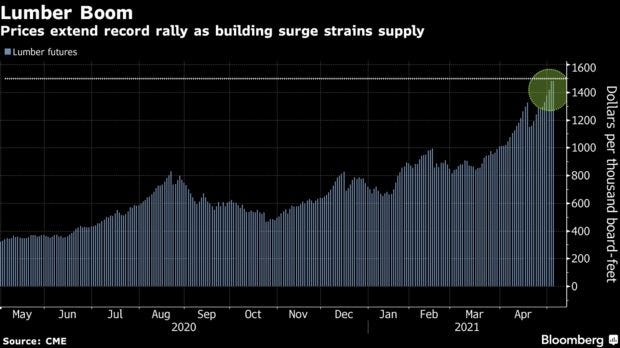

Inflation to Rise, Unemployment to Fall

And are we seeing any signs of inflation as we reopen?

Many folks will proclaim, that these are temporary blips. That, despite large doses of fiscal and monetary actions in the past year, sustained inflation is yet to be seen and nowhere close. It’s worth reminding them that the past year also happened to have one of the most rapid and intense onset of deflationary macroeconomic headwinds in modern history which are already starting to rapidly reverse.

Unlike other causes of deflation (such as the great depression or 2008 financial crisis), reactivation of large segments of the economy is something that can occur on the order of weeks like the flip of a switch—just as shutting down the economy occurred:

Lumber and real estate is just one segment. The rebound from reopening is set to be rapid, massive and, due to non-linear, multi-order effects and feedback loops, it is irresponsible for any investor to dismiss the risk of unrestrained inflation in the coming months.

And the Fed will not have to worry about rising rates affecting employment if excess capacity is soaked up by surging demand. And American consumers certainly have a lot of dry powder ready to deploy:

If you are skeptical about coming inflation, you are betting that Americans have permanently changed their consumption habits (committing the folly of “This Time is Different”)…

Instead, as Buffett said—we ask: “And now what”?

So you're saying there is obvious inflation resulting in asset prices falling due to increased rates