Bloodletting of Bear Markets I: Mandelbrot's Fractal Turbulence & Volatility Clustering

Bloodletting of Bear Markets I: Mandelbrot's Fractal Turbulence & Volatility Clustering

Volatility Begets Volatility: Part of a Series Highlighting Downside Risk

"Large changes tend to be followed by large changes, of either sign, and small changes tend to be followed by small changes."

— Benoit Mandelbrot, “The Variation of Certain Speculative Prices” (1967)

Fintwit’s never-ending obsession with short term market moves and recent disruptions in longstanding trends has brought to the fore some interesting discussions.

Lately, markets put up all time highs only to be followed by, in quick succession, a sudden rise in treasury bond yields causing a steep selloff in technology stocks which have led the equity rally of the last decade or so (as I highlighted a couple of weeks ago, equities, especially technology issues of today, are highly sensitive to interest rates).

Twitter’s tendency to shorten attention spans will not bode well for many Fintwit followers. With recently complacent markets that have stuck within clear trend lines (more “predictable” market behavior), there has been a rise of trading accounts that have thrived on short term trading predictions. The accounts get more attention and followers the more “correct” they have proven with forecasting…

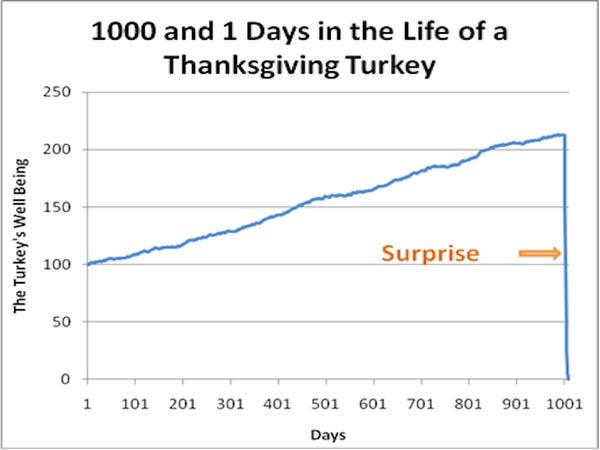

Eventually however, a shock is bound to occur and the strategy revealed to be fragile. As Nassim Taleb illustrated in “The Black Swan” in the life of a Thanksgiving turkey:

Now it seems there are cracks in the reputations of Fintwit traders as a few have been caught flat-footed by the recent deviation from trend. An opening has emerged to call out flaws in their claims:

When there is a reversal in a trend and what once worked inevitably loses its magic, the soothsayers once heralded as prophets lose their luster. Their strategies (and reputations) proved fragile over the course of time.

Imagine what happens when a thus far “successful trader” builds a large following on Twitter. The number of folks following that individual’s moves (and the number who are following the followers) grows with each success. Eventually, when Thanksgiving comes, all experience losses and many attempt to flee their positions at once, causing a feedback loop that exacerbates the “deviation” from that trader’s strategy and increases the magnitude of losses.

Interestingly, in one of the attempts to rebut the above tweet and support those who forecast markets, a startling claim is made about Benoit Mandelbrot:

Mandelbrot spent an inordinate amount of time studying market dynamics of pricing—not just for stocks, but assets such as cotton and currencies. As @macrocephalod highlights, Mandelbrot’s main accomplishment in this arena was concluding that models based on Brownian motion did not capture real market behavior very well:

Mandelbrot used models grounded in fractal dynamics which still relied on underlying movements that were random. In “The Misbehavior of Markets”, Mandelbrot attempts to create an artificial series of price changes that mimics real world market observations based on such modeling. Mandelbrot never claimed markets are “not random”.

Though Mandelbrot’s method of modeling markets never took off, it is insightful nonetheless to review Mandelbrot’s Ten Heresies of Finance found in Chapter 12 of “The Misbehavior of Markets”. These are valuable notions from someone who has experienced and closely studied a variety of markets. Understanding them is crucial to understanding how one ought to think of markets from a 10,000 foot view. They all are (with my comments in parentheses):

Markets Are Turbulent. (There are feedback loops, volatility begets volatility which in part lead to “bursts and pauses” in markets “whose parts scale fractally”)

Markets Are Very, Very Risky—More Risky Than the Standard Theories Imagine. (Gaussian “bell curve” doesn’t work, the risk explains the equity risk premium, big drops hurt a lot for a long time and risk of ruin must be accounted for)

Market “Timing” Matters Greatly. Big Gains and Losses Concentrate into Small Packages of Time. (Think $GME of late)

Prices Often Leap, Not Glide. That Adds to the Risk. (Again, feedback loops—for example, contagion; volatility leading to more: acceleration; price moves have discontinuity incompatible with classical physics)

In Markets, Time is Flexible. (Scaling property that comes from fractal dynamics: zooming in on a 1m chart looks awfully similar to a 1d chart or a 1y chart)

Markets in All Places and Ages Work Alike. (Don’t kid yourself with ‘This Time is Different’)

Markets Are Inherently Uncertain, and Bubbles Are Inevitable. (Think about this when observing the bravado of the latest “hot” forecasters who trade on Twitter; Or “Buy the Dip” mentality and bubble risk)

Markets Are Deceptive. (Think about this when Fintwit makes claims as to why the market does what it does; think about those who subscribe to technical analysis and charting)

Forecasting Prices May Be Perilious, but You Can Estimate the Odds of Future Volatility. (pricing not predictable, but if you are in volatile waters, there is a good chance you may be in a cluster—be cautious when the storm clouds gather)

In Financial Markets, the Idea of “Value” Has Limited Value. (Value is “a slippery concept…whose usefulness is vastly over-rated”—think of the “value investors” who have substantially underperformed the last decade)

Takeaway

Attempts to describe, narrate, and predict markets have been made over the ages by pundits via old and new forms of media. Don’t fall for it. Today’s social media adds a new dimension to this phenomenon and a shortening of attention span leaves one prone to misunderstand the true risks of their exposure. It’s best to not lose sight of how markets have behaved throughout the ages and the fact that the season can quickly change.

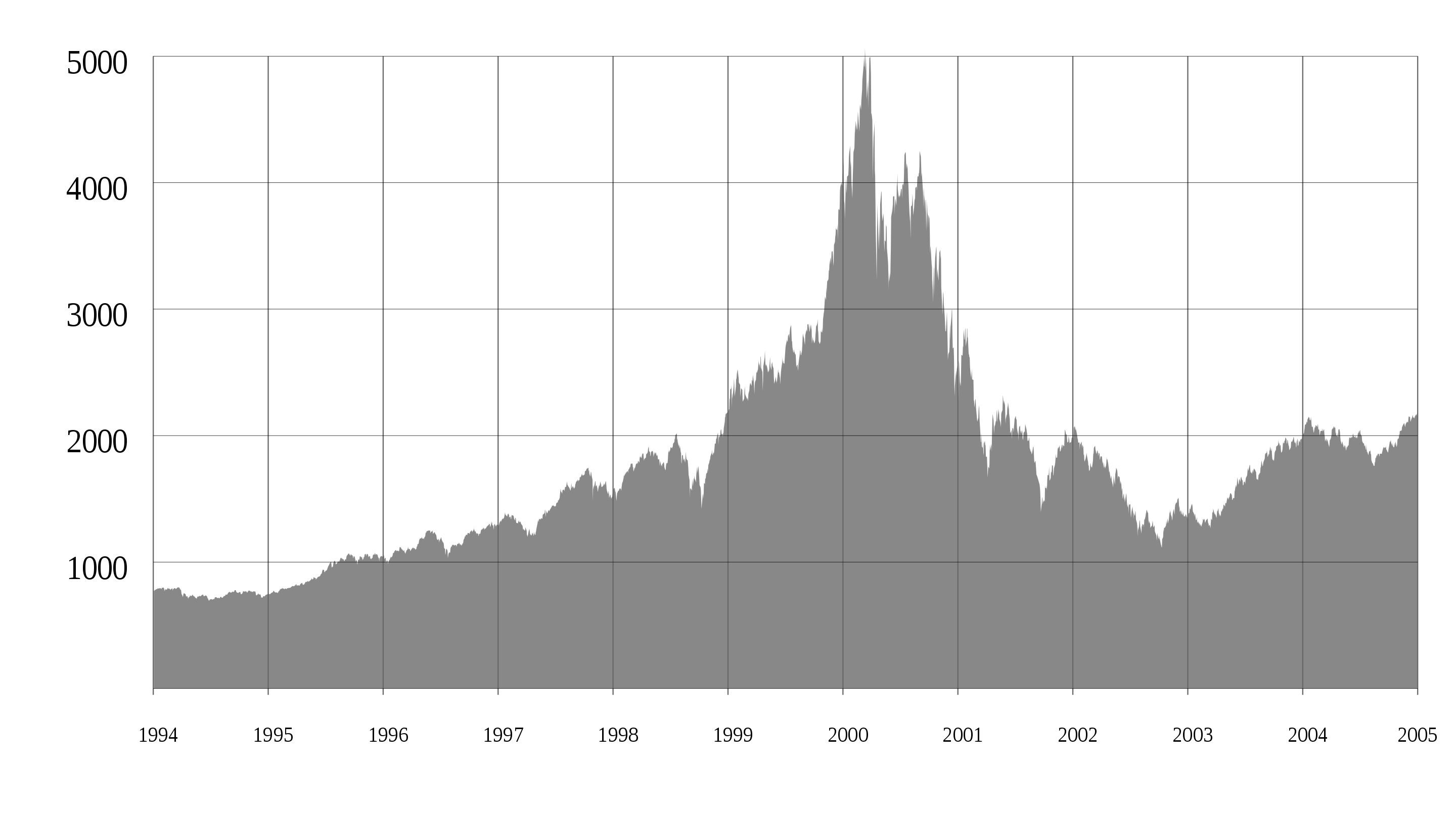

In order to help meditate on the above, here’s a chart of the Nasdaq from 1994 to 2005: